Enter your brand or company name to get started.

Every business idea needs to be researched, planned, financed, registered, insured, and promoted before it becomes a reality. If you can work through each of the appropriate steps without cutting corners, you can emerge with a profitable business that you can be proud of.

Business Plan Template — Free Download

Use our free business plan template to get a head start on your business preparations.

Download NowHow to Start a Business:

Starting a business is hard work, but it might be easier than you think. Start-up costs vary depending on the size, location, and type of business, and the internet has made it relatively easy to start a business these days. Follow these steps and you'll be able to launch your own small business with confidence.

Do market research.

Research using a variety of methods.

No matter how good you think your idea is, you need to find out what the market is saying about it. Entrepreneurs who are too close to their idea can become so convinced that it will be a success that they forget to look beyond themselves for confirmation. This can lead to a disappointing outcome.

Market research can be conducted in a variety of ways, including:

- Conducting surveys.

- Reading literature from economic studies.

- Studying competitors.

- Passing out samples of your product.

- Analyzing demographics.

The two types of market research are primary and secondary. Primary market research comes from direct interaction with customers. Secondary market research is garnered from studies, reports, statistics, and other data that you can source from a third party.

You can conduct market research yourself, or you can hire a consulting firm to do the research for you. Obviously, doing the work in-house will save you a lot of money. Since most people who are starting a business don't have much capital, this is the most popular option. Consulting firms are generally only brought in when the entrepreneur has readily available access to funding, or they are considering a move into a very specialized or highly competitive space.

Create a business plan.

Focus on potential investors.

One of the most important reasons to have a business plan is that it will help you get funding. Investors and lenders will want to know exactly where their money is going and what the prospects of a return on their investment are. Because of this, the market research that you have compiled is a key piece of the business plan.

Try your best to be both detailed and concise when you are creating your business plan. It's best to avoid technical jargon and industry terms that an outside investor might not understand. If you have to use these terms to get your point across, make sure you explain them.

Write an executive summary.

Although the first item that you need to include is the Executive Summary, it might be easier for you to write it last. After you have created all of the other parts, it will probably be easier for you to summarize the business and your plan for how to start it.

Secure financing.

Decide which type(s) of financing you need.

There are a variety of ways to fund your business. You can borrow money from friends or family and offer to pay them interest, you can secure a small business loan from a bank or qualified lender, you can sell equity in your company, or you can apply for local and State small business grants. Crowdfunding is becoming a popular way to raise money.

Prepare the right documentation.

If you choose to take the traditional route and apply for a small business loan, most lenders will require the following:

- A good credit score.

- Collateral to post against the loan (property, assets, etc.).

- A two-year history of your income.

Obtaining a loan for a new business is usually harder than obtaining one for an existing business because the lender does not have as much information to go on, so interest rates are usually higher.

SBA loans are a popular choice for entrepreneurs because they are guaranteed by the government. SBA loans were created to encourage small business development and are therefore easier to qualify for than private loans.

Consider selling equity in your company.

Many business owners are reluctant to sell equity in their company because they want to maintain complete ownership.

By splitting ownership in a young company too many ways, you dilute its value and risk losing the equity that will one day make you wealthy. At the same time, you might need partners who can help you get your business where it needs to go. Most of all, you probably need money to invest in your business.

If you're having difficulty getting the loans or the credit that you need, selling equity could be a good option. Just remember that whoever buys equity is also entitled to a share of the profits.

Create a legal entity.

Choose a legal structure.

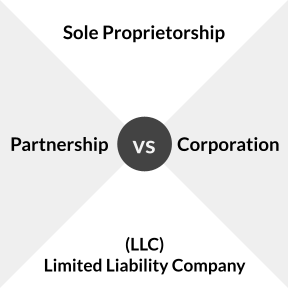

The four most common legal structures for a small business are:

Sole proprietorship: includes only one person who is the owner/operator of the business. There are no employees and all profits are the proprietor's personal income. The sole proprietor personally assumes all liability for the business. You'll likely need to use a schedule C form to report profits and losses.

Partnership: a business relationship between two or more people who share costs and revenues. Partnerships do not pay income tax but must file an annual return. Taxes are passed on to the individual members of the partnership.

Corporation: a corporation is a standalone entity with shareholders. A corporation must file an annual tax return and is required to pay corporate taxes.

Limited Liability Company (LLC): LLCs are regulated by State laws. An LLC can be owned by a person, persons, or a corporation. Depending on the size and location of the LLC, it may be treated as a partnership or corporation for tax purposes. Check your State's laws for more information.

The way that you choose to set up your business is up to you, but it will probably have a lot to do with how similar companies in your industry are structured. As your business grows, you can create a new kind of entity if necessary.

Register with the Secretary of State.

Income from a sole proprietorship can be reported on your personal income tax return, but corporations and LLCs need to be registered. The process for registering in each state is slightly different, but you need to provide the following:

- A registered agent, i.e., the company representative with a physical address in the State of incorporation.

- Names and addresses of officers, directors, and members.

Apply for an EIN.

If you have employees, you also need to register for an Employer Identification Number (EIN) with the IRS. You can apply online at IRS.gov.

Find a location for your business.

Choose between leasing and purchasing a property.

It is unusual for someone who is starting a business to buy a property right away, but it may be necessary if your business needs the property to generate revenue.

For example, a self-storage business needs a piece of property with storage units on it in order to make money. If your business only needs a small office or storefront, renting is a much better financial option when you are starting out.

Decide what kind of space you need.

Determine where you would like your business to be located and then start shopping for commercial real estate. You can buy a property, or rent an office, store, or warehouse.

If you're unfamiliar with local real estate, working with a real estate agent could be very helpful.

Purchase insurance.

Find out which type of insurance you need.

There are many different types of small business insurance that you can purchase, including:

- Property insurance: covers damages to your business's property.

- Liability insurance: protects your business from legal liability if your service or product causes harm.

- Professional liability insurance: protects professional service providers against civil lawsuits associated with their service.

- Health insurance: covers or partially covers you and your employees' medical bills.

- Automobile insurance: for single or multiple-vehicle coverage. Available for vehicles that are used for business purposes.

- Cyber insurance: coverage that kicks in in the event of a cyberattack that destroys your data or steals your customers' information.

- Business interruption insurance: available to supplement a sudden loss of income when circumstances beyond your control cause your business to shut down for a period of time.

Most small business insurance providers can bundle different types of coverage to save your business money. You can also customize your coverage limits and deductibles to create a policy that is affordable and appropriate for you.

If you don't want to contact insurance companies directly for a quote, you can contact an insurance broker. A broker will negotiate on your behalf to find you the best deal, and you don't have to pay them anything because they earn sales commissions from the insurance company that you sign with.

Hire employees.

List what positions need to be filled.

Before you start advertising job opportunities, figure out exactly how many employees you need and what positions you need them to fill. Common jobs include:

- Cashier.

- Customer service agent.

- General laborer.

- Secretary.

- Administrative assistant.

- Manager.

Post job opportunities.

The fastest way to advertise job opportunities is to post them online using job sites like Indeed. You can also use job posting software like Betterteam to post jobs to hundreds of sites instantly and manage applications as they come in.

Be sure to include a detailed job description in your job posting so that people know exactly what they are applying for.

Review applications.

As people send in their resumes and cover letters, you can read through them and separate qualified applicants from unqualified ones.

Schedule interviews.

Once you have found enough suitable candidates for the job(s) that you are hiring for, reach out to them and schedule in-person interviews. These interviews will allow you to meet the candidates and further assess their ability to meet your business's needs.

Send out job offers.

Once you're prepared to bring the best candidates on board, send out formal job offers to each of them that include a possible start date, their rate of pay, and their official title.

Once you have hired a new employee, make sure that they fill out a W-4 form and return it to you so that you know how much taxes to withhold from their paycheck. They also need to fill out IRS Form I-9, declaring their eligibility to work in the United States.

If you are hiring workers for skilled positions, make sure that they either have the appropriate training or that you can provide it on the job.

Develop business relationships.

Network with key players.

When you approach a supplier as a business, you bring value because you represent the possibility of becoming a long term customer. A good business-to-business relationship is mutually beneficial because it gives long term stability to both parties.

Join your local chamber of commerce.

One great way to develop relationships with other businesses in your area is to attend networking events. If you join your local chamber of commerce or business association, you will have the opportunity to attend networking events where you can meet other business owners.

Don't forget that you can do a lot of your networking online with professional social media platforms like LinkedIn.

Brand and advertise.

Write an elevator pitch.

One of the cornerstones of successful marketing is a compelling elevator pitch. An elevator pitch is exactly what it sounds like - a very brief summary of what your business is and why it is valuable. A good elevator pitch should grab the attention of investors and customers. It can also be your point of reference when you are branding products or services.

Create a brand identity.

Before you start advertising, you need to create a brand identity. To do this, ask yourself questions like:

- Who are my customers?

- What problem does my business solve?

- What do my customers want?

- Is my value proposition unique?

- What kind of personality should my brand have?

- What feelings do I want to be associated with my brand?

- How do my competitors position themselves?

Design a logo.

A logo makes your business instantly identifiable. If you have design skills, you can create your logo, but you can also hire a graphic design or logo design service to create a professional logo for your business.

Try Zarla's free logo maker to create, edit, and download a unique logo for your business.

Build a website and social media accounts.

A website and an active social media presence are essential in today's digitally-driven marketplace. You can use an AI website builder such as Zarla to build your own website or hire a web design agency.

Setting up social media accounts is very easy and 100% free. Create business pages on platforms like Facebook, Twitter, and LinkedIn.

Make sure that your social media accounts and your website are linked.

Zarla will ask you for some details then will set up your website with a business description and list of services in seconds.

How to Start a Business — Free Checklist

Use this PDF checklist to guide you through each step of starting your own business.

Download Now

How to Create a Brand Identity